- Cmind AI by Weihong Zhang

- Posts

- NVDA at 85%: The AI Trade Faces Its Next Earnings Test

NVDA at 85%: The AI Trade Faces Its Next Earnings Test

Cmind sees a Very Likely Beat, but the late pullback from ~99% makes guidance, Blackwell, margins, and post-print dispersion across INTU, ZM, ADI, TJX, IQ, HD, and small-cap tech.

Weihong Zhang

May 18, 2026

Cmind Earnings Edge — Week of May 18 - 22, 2026

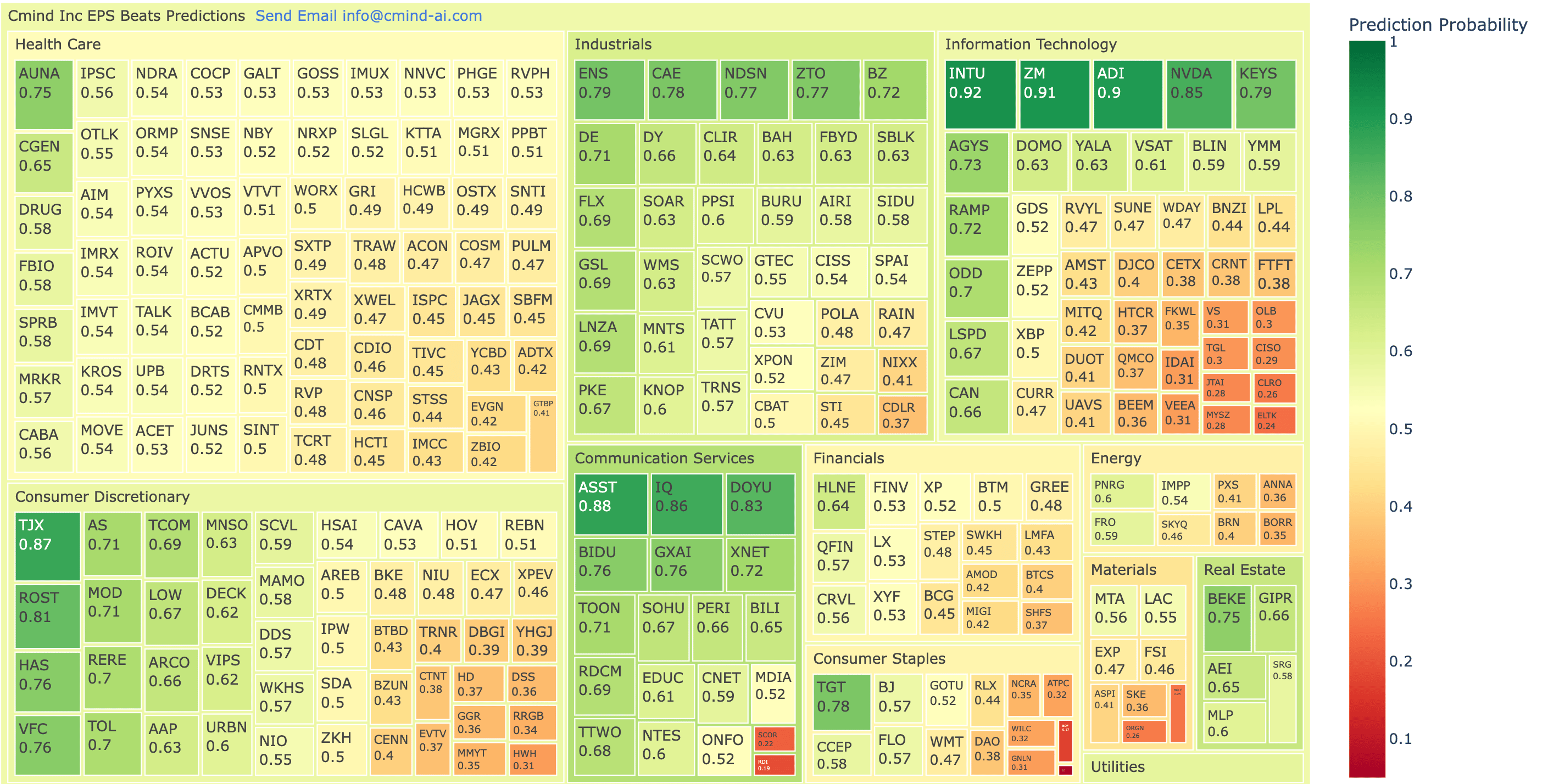

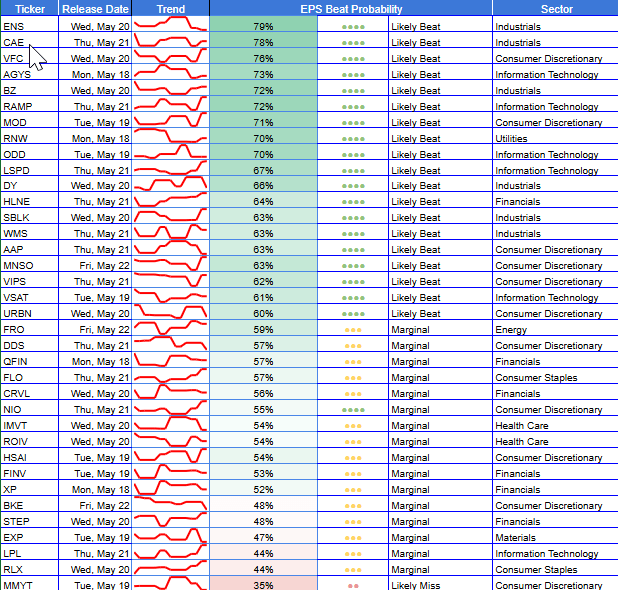

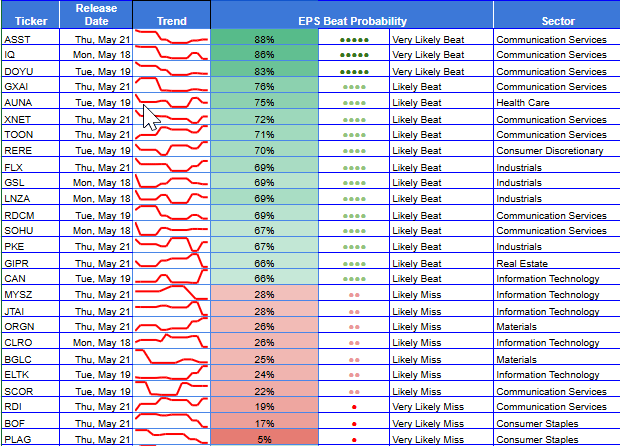

Cmind’s active May 18–23 heatmap captures 278 model-tracked names with an average beat probability of approximately 52.5%. About 58.6% of the universe carries a beat label, but only 10.8% screens above the 70% high-conviction threshold, while 16.9% sits below the 40% miss-risk threshold. That distribution points to a basket-construction week, not a beta week: large caps screen materially stronger than small caps, Information Technology contains both the most important beat signals and the weakest downside tail, and Consumer Discretionary shows a clear split between resilient retailers and housing-sensitive risk.

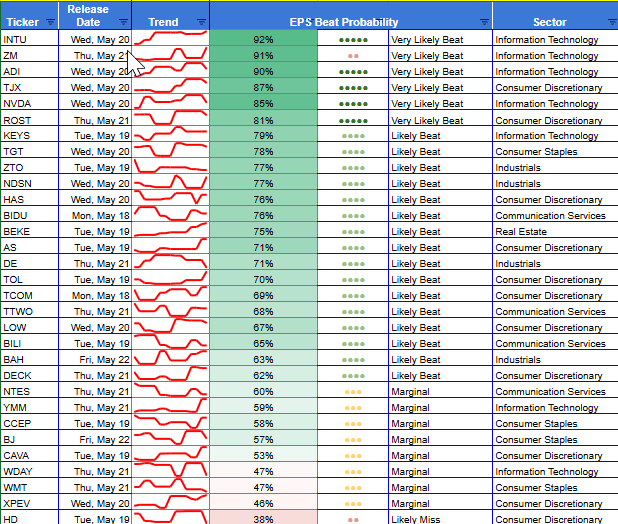

The Feature of the Week is Nvidia ($NVDA). NVDA reports on May 20, with consensus EPS of $1.70, following prior-quarter actual EPS of $1.57 versus prior consensus of $1.45. Cmind assigns NVDA an 85.2% beat probability and a Very Likely Beat classification. The signal is still high conviction, but the late reset from the early-May peak near 99% makes the event more nuanced: the model supports beat risk, while the post-print reaction likely depends on Data Center growth, Blackwell ramp commentary, gross margin durability, AI demand breadth, and whether management can clear an already elevated investor bar.

This week’s signal map: INTU, ZM, ADI, TJX, IQ, and NVDA anchor the beat side; HD is the most important large-cap negative revision; and the sharpest probability moves — including TOON, MDIA, EDUC, WILC, HD, and NTES — point to a market where pre-print revisions may matter as much as the final score.

Feature of the Week: NVDA — High-Conviction Beat, High-Bar Event

Nvidia is the most important earnings event of the May 18–23 window because it is no longer just a semiconductor print. It is the market’s cleanest real-time referendum on the durability of the AI infrastructure cycle. For hedge funds, systematic equity teams, and options desks, the core question is not simply, “Will NVDA beat EPS?” Cmind’s model already leans strongly positive. The more important question is whether Nvidia can deliver a beat-and-guide that extends the AI trade rather than merely validating expectations already embedded in the stock and the broader AI complex.

Cmind currently assigns NVDA an 85.2% beat probability and a Very Likely Beat classification. The setup is constructive, but not one-dimensional. The model’s driver set maps directly to the variables institutional investors are already underwriting: profitability, gross margin change, operating leverage, asset efficiency, inventory posture, cash-to-operating-profit dynamics, analyst sentiment, CFO sentiment, and capitalized-expense intensity. That matters because it suggests the signal is not being driven by one narrow AI narrative; it is supported across operating, balance-sheet, and language-based inputs.

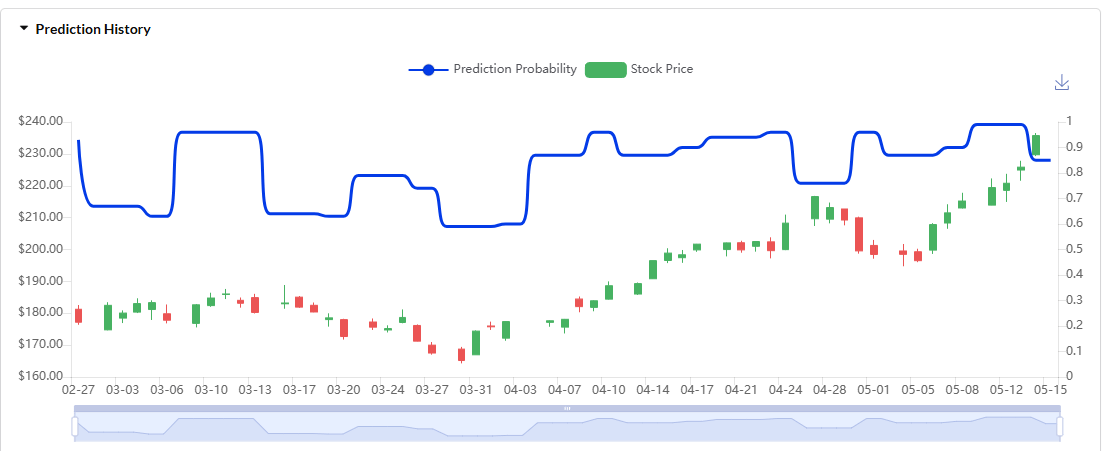

The revision path is the key nuance. NVDA began the forecast cycle with a very high beat probability, then temporarily fell into the low-to-mid 60s during March. The first major rebound came on March 7, when the probability jumped to roughly 95.7%, before fading again later in the month. By late March and early April, the signal bottomed around 59–60%, but the beat call did not break. It then rebuilt sharply into the high-80s and stayed mostly above 90% from April 9–24. Confidence peaked near 99% from May 9–13 before resetting to 85.2% on May 14–15.

That pattern should be framed as bullish, but not complacent. The late pullback from nearly 99% to 85.2% does not look like a bearish reversal. It looks more like expectation-risk adjustment after the model reached extreme confidence. For event-driven and options investors, that distinction is important. A high beat probability supports a constructive earnings setup, but NVDA is a high-bar event where the stock reaction may depend more on forward commentary than on the EPS print itself.

Investors will likely focus on five areas. First, Data Center growth: whether demand is still broadening beyond the first wave of hyperscaler AI infrastructure buyers. Second, Blackwell ramp commentary: timing, supply availability, customer adoption, and margin implications. Third, gross margin durability: whether incremental AI demand still converts into operating leverage. Fourth, AI ROI: whether customers are still spending aggressively because deployment economics are improving. Fifth, second-order read-throughs: whether the print supports adjacent names such as ADI, KEYS, INTU, ZM, networking, test-and-measurement, software automation, and other AI-adjacent beneficiaries.

This is why NVDA matters beyond NVDA. A strong print and guide would likely reinforce the idea that AI capex is still converting into revenue, margin, and backlog across the ecosystem. That would support not only semis, but also analog, test-and-measurement, enterprise software, cloud-adjacent infrastructure, and AI-enabled productivity names. A weaker guide would challenge the assumption that AI spending is still compounding smoothly, and the risk would not be limited to Nvidia. It could pressure the broader AI basket, especially names where positioning has outrun visible monetization.

The relative setup inside Technology also matters. NVDA is one of the highest-quality large-cap tech signals in the heatmap, but it is not alone. INTU screens at 92.1%, ZM at 90.6%, ADI at 89.9%, and NVDA at 85.2%, creating a high-conviction large-cap tech cluster. At the same time, the lower-quality tail of small-cap Technology screens weak, with names such as ELTK, CLRO, VEEA, CISO, IDAI, and FTFT sitting in lower-probability zones. That makes Technology the most important dispersion sector of the week, not a uniformly bullish sector call.

NVDA remains a high-conviction Cmind beat signal, but the trade is no longer simply “beat or miss.” It is beat quality, guidance quality, AI capex durability, and the next 30 days of dispersion across the AI ecosystem.

Heatmap

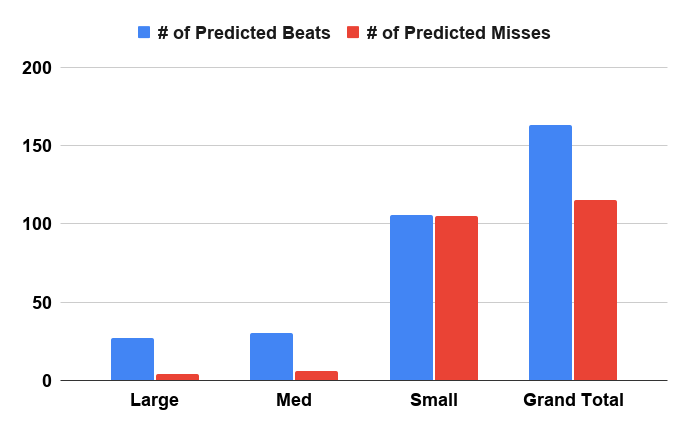

Cmind’s May 18–23 heatmap shows a market where the strongest signals are concentrated rather than broad-based. The large-cap cohort is materially stronger than the rest of the universe, while small caps carry the widest miss-risk tail.

Market Cap Exposure

Mega / Large Cap

Large caps are the cleanest cohort. The large-cap group has an average beat probability of approximately 68.8%, with 87.1% of names carrying a beat label and 51.6% above the 70% threshold. Key large-cap beat signals include INTU, ZM, ADI, TJX, NVDA, TCOM, BIDU, TOL, HAS, ROST, VFC, DE, ZTO, and KEYS. For PMs, this supports using large-cap quality names as the long side of an earnings basket.

Mid Cap

Midcaps are positive but more selective. Midcaps average roughly 60.2%, with 83.3% beat-labeled and 19.4% above the 70% threshold. Notable midcap signals include AGYS, MOD, BZ, VFC, SBLK, HSAI, and SBLK. This is a more tactical cohort where individual revision paths matter more than sector labels.

Small Cap

Small caps remain the highest-risk zone. Small caps dominate the active heatmap, but the average probability is only 48.8%. Just 3.3% of small caps screen above 70%, while 21.3% fall below the 40% miss-risk threshold. This is where liquidity, balance-sheet risk, and sentiment instability matter most.

Sector Exposure

Communication Services is one of the strongest sector clusters, with an average probability of approximately 63.7%. ASST, IQ, DOYU, BIDU, GXAI, XNET, TOON, SOHU, and BILI screen positively. The sector is especially relevant because it combines China's internet, digital media, gaming, and ad-market exposure.

Industrials also screen well, with an average probability of around 60.0%. ENS, CAE, NDSN, ZTO, BZ, DE, DY, CLIR, BAH, SBLK, and FLX contribute to the positive read. This is a useful cyclical confirmation group, especially if investors are looking for earnings breadth beyond AI semis.

Information Technology is the most important sector, but not uniformly strong. The average probability is only 49.3%, yet the top of the sector is extremely relevant: INTU, ZM, ADI, NVDA, KEYS, AGYS, and RAMP. The weakness sits in the long tail of smaller IT names such as CLRO, ELTK, VS, IDAI, VEEA, CISO, and FTFT. This is classic dispersion: high-quality AI/software/semiconductor names screen well, while lower-quality, smaller tech screens poorly.

Consumer Discretionary is mixed but important. TJX, ROST, HAS, VFC, AS, TOL, MOD, TCOM, LOW, and DECK screen positively. However, HD, RRGB, HHH, MMYT, and several smaller discretionary names sit in weaker zones. That creates a relative-value setup around consumer resilience: off-price/apparel and select travel/auto-related names look stronger than big-ticket housing-sensitive spend.

Consumer Staples, Materials, Energy, and Financials carry more caution. Consumer Staples averages only 41.6%, Materials also sits near 41.6%, Energy averages 46.5%, and Financials average approximately 48.8%. These are not broad short signals, but they are clear areas where the heatmap shows weaker beat support and more miss-risk density.

Top 6 Beat/Miss Signals - Week of May 18, 2026

Top 6 Beats

Ticker | Company | Announces | Sector | Market Cap | Beat Probability |

INTU | Intuit Inc. | May 20 AMC | Information Technology | Large / $209.9B | 92.1% |

ZM | Zoom Communications | May 21 AMC | Information Technology | Large / $22.6B | 90.6% |

ADI | Analog Devices | May 20 BMO | Information Technology | Large / $120.0B | 89.9% |

ASST | Strive, Inc. | May 21 Midday | Communication Services | Small / $75M | 87.8% |

TJX | TJX Companies | May 20 BMO | Consumer Discretionary | Large / $136.3B | 86.5% |

IQ | iQIYI | May 18 BMO | Communication Services | Small / $1.9B | 85.6% |

NVDA sits just outside the top six at 85.2%, but it is the most market-relevant signal because of its index weight, AI leadership, and read-through to the broader AI capex trade.

Top 6 Misses

Ticker | Company | Announces | Sector | Market Cap | Beat Probability |

PLAG | Planet Green Holdings | May 21 Midday | Consumer Staples | Small / $9M | 5.1% |

BOF | BranchOut Food | May 21 Midday | Consumer Staples | Small / $26M | 17.4% |

RDI | Reading International | May 21 Midday | Communication Services | Small / $42M | 19.3% |

SCOR | comScore | May 19 Midday | Communication Services | Small / $27M | 22.2% |

ELTK | Eltek Ltd. | May 19 BMO | Information Technology | Small / $69M | 24.1% |

BGLC | BioNexus Gene Lab | May 21 Midday | Materials | Small / $9M | 25.3% |

Top Movers: Largest Probability Shifts

Upward Movers

TOON: 25.3% → 70.6% /+45.3 pts.

The largest positive reset, moving from miss-risk territory into a clear beat profile.

MDIA: 18.1% → 52.3% /+34.3 pts.

A major communication services recovery, though still closer to marginal than high-conviction.

EDUC: 27.3% → 61.3% /+34.0 pts.

Strong positive revision, with inventory, margin, and CFO-related features likely contributing.

CNET: 27.3% → 59.0% /+31.7 pts.

A meaningful improvement into the print, but still below the 70% high-conviction threshold.

SIDU: 26.5% → 57.6% /+31.1 pts.

A sharp small-cap Industrials upgrade, useful as a sentiment/microcap dispersion marker.

SKE: 7.2% → 36.2% /+29.1 pts.

Still below neutral, but no longer in the extreme miss-risk zone.

More liquid positive revisions to watch: ZM +20.7 pts, TOL +20.6 pts, INTU +16.0 pts, BEKE +14.5 pts, and TJX +12.3 pts.

Downward Movers

WILC: 73.0% → 31.7% /-41.3 pts.

The largest negative reset, moving from beat territory into miss-risk.

HD: 77.2% → 37.5% /-39.7 pts.

The most important negative large-cap revision and a key housing/consumer signal.

GGR: 73.4% → 36.3% /-37.1 pts.

Consumer discretionary risk increased sharply into the print.

NTES: 94.6% → 59.6% /-34.9 pts. Still above neutral, but a major de-risking in China internet/gaming.

DAO: 69.6% → 37.8% /-31.9 pts.

A sharp consumer/education-related reset.

SCWO: 88.6% → 57.2% /-31.4 pts.

Industrials beat confidence faded significantly.

More liquid negative revisions to watch: WDAY -25.0 pts, TTWO -24.9 pts, BILI -20.0 pts, WMT -15.9 pts, and HAS -15.1 pts.

30-Day Setup

The next 30 days should be treated as a dispersion regime, not a broad directional regime. NVDA is the central event, but the better systematic opportunity may be in the second-order baskets.

A strong NVDA report would likely reinforce INTU, ZM, ADI, KEYS, RAMP, AGYS, and other AI-adjacent software, semiconductor, networking, and test/measurement names. A weaker guide would matter beyond NVDA because it would challenge the assumption that AI capex is still converting smoothly into revenue, margin, and forward demand.

The cleanest relative-value setup is within Technology: high-probability large-cap tech names such as INTU, ZM, ADI, NVDA, and KEYS versus weaker small-cap IT names such as CLRO, ELTK, VEEA, FTFT, IDAI, and CISO. In Consumer Discretionary, the model flags a sharp contrast between stronger names such as TJX, ROST, TOL, MOD, and TCOM and the negative revision in HD.

Recap

This week’s tape is not index-led. It is catalyst-led, factor-led, and dispersion-led.

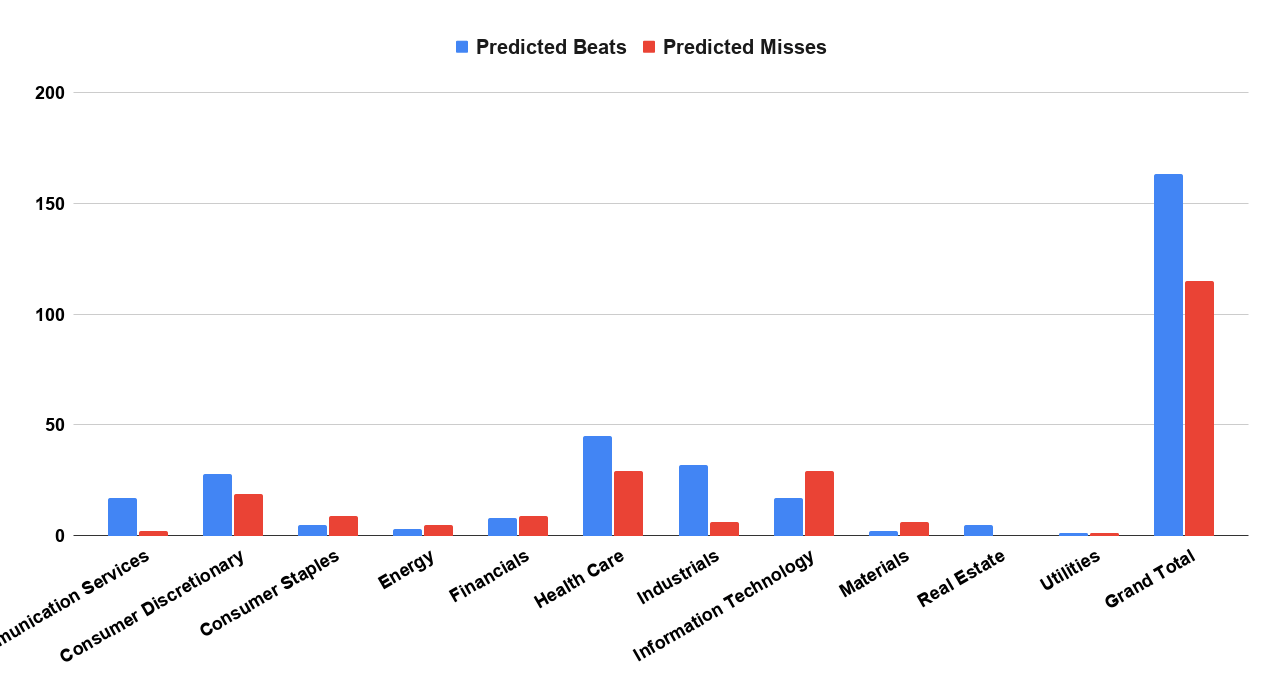

The strongest large-cap signals are concentrated in Information Technology and Consumer Discretionary, led by INTU, ZM, ADI, TJX, and NVDA. Communication Services offers meaningful upside through IQ, BIDU, DOYU, and ASST, while Industrials provide additional breadth through ENS, CAE, NDSN, ZTO, BZ, and DE.

The key risk zones are small-cap Technology, Consumer Staples, Materials, and weaker pockets of Consumer Discretionary. The most important single-name risk signal is HD, where Cmind shows a sharp downward revision into the print.

For systematic and quantamental investors, the opportunity is not simply identifying who may beat. It is isolating to see the model signal probability revisions, sector divergence, and potential post-print drift before the market fully reprices the next leg of the earnings narrative.

About the Model

Cmind AI’s EPS predictions are powered by a machine learning model built for accuracy, objectivity, transparency, and daily updates with the latest market information. We ingest over 150 variables across five data modalities—including real-time 10-Q filings, earnings transcripts, governance metrics, and peer signals—to provide early, company-specific EPS forecasts.

Our EPS signals are updated daily across 4,400+ U.S. stocks using a multi-input ML model (filings, transcripts, price-to-earnings dynamics, governance, and peer signals). The goal isn’t to predict headlines—it’s to quantify where dispersion is most likely so you can build better baskets, hedges, and sizing into catalyst windows.

📩 To learn more, contact us at [email protected].